Balancing the Costs and Value of Graduate Programs

Introduction

As student debt levels continue to rise, policymakers, borrowers, and families are asking questions about the value of higher education, including whether their credentials will pay off enough down the line to justify the rising costs. To date, much of the conversation has focused on undergraduate education. However, borrowing for colleges that increasingly charge exorbitant prices for advanced degrees — mainly master’s degrees and professional programs — warrants much more attention.

Today, graduate debt makes up a large — and growing — share of the $1.6 trillion federal student loan portfolio. The Department of Education’s Office of the Chief Economist projects that soon, half of all federal student loan dollars issued annually will go to graduate students, though such students make up just 21 percent of federal student loan borrowers.1 This is a significant shift. In the year 2000, for example, graduate loans made up roughly 30 percent of federal student loan dollars.2 The cumulative debt for graduate school students increased by about 25 percent over roughly the same timeframe.3 Growing graduate school enrollment, along with the rising cost of graduate school, have led to these significantly higher debt levels for graduate borrowers. 4

≈46%

of all federal loan dollars were made up of graduate loans in the year 2025.

While some graduate programs pay off for students, far too many ultimately do not. The Education Department’s Office of the Chief Economist found that, across most sectors of higher education, those who graduate from the lowest-performing 10 percent of graduate programs typically earn a full $50,000 less than graduates from the highest-performing 10 percent of programs. 5 While students are paying more — and borrowing more — for graduate education, they are not seeing an equivalent increase in the value of their degrees.

Colleges have every incentive to grow their graduate programs and raise their prices, regardless of the value to the graduates. Many institutions have found they can generate increased revenue from a fast-growing number of graduate programs, many of which do not provide enough value in the labor market to justify the costs. 6 Further, unlike undergraduate loans, graduate lending is capped only at the price of attendance — a figure set by the school — so colleges are further motivated to grow the size of their programs as they raise their prices to generate even more revenue.

At the same time, policymakers have expanded graduate borrowers’ access to increasingly generous student loan repayment plans, further enabling colleges to charge high prices. The growth of income-driven repayment plans have allowed graduate borrowers to reduce their repayments considerably and to see sizable balances forgiven after 20 or 25 years — a notable shift compared with other (fixed) repayment plans that require borrowers to pay back the full amount they borrowed, plus interest. 7Given this reality, the share of borrowers repaying their loans in full is projected to decline — and Grad PLUS loans, which the Congressional Budget Office once scored as saving the government billions each year, now cost the government money. 8

This confluence of growing debt, uneven returns, and ballooning costs has caused many policymakers to take note. The time is ripe to reconsider how the student loan programs can better serve students — and whether students and taxpayers are paying the price for programs that charge too much and provide too little.

About Graduate Student Loans

Today, graduate student loan borrowers may take up to $20,500 each year in Graduate Stafford loans — the same types of loans available to all undergraduate students at lower limits. Graduate students may also take on Grad PLUS loans, which were created by Congress in 2005. These loans are capped only by the cost of attendance for the program, which is set by the institution. Grad PLUS loans carry higher origination fees and interest rates than Graduate Stafford loans. 9 Just 28 percent of graduate borrowers had a Grad PLUS loan, though graduate school loans (including Graduate Stafford loans) make up 46 percent of annual student loan volume. 10

25%

increase in cumulative graduate student debt since 2000.

By the Numbers

More students are going to graduate school — but they are not always seeing the earning benefits of those degrees. Particularly since the Great Recession, more students are pursuing master’s degrees and other graduate education. The graduate-degree attainment rate has increased much faster for women than men, including for Black and Hispanic women. 11 Yet the Chief Economist of the Department of Education found that, while the so-called ‘earnings premium’ to a graduate degree, particularly relative to a high school graduate, is strong, these earnings increases have flattened in recent years as students needed to borrow more to pay for those programs. Even within the same field, there is considerable variation in the returns that graduates see from college to college. 12

Borrowers are taking on higher levels of debt for graduate education. On average, graduate school borrowers took on more than $66,000 in loans for their graduate education in 2016. This is about a 25 percent increase since 2000, when that average was about $53,000. 13 Often, borrowers take on more debt because prices have increased. For instance, a report from the American Enterprise Institute, The Century Foundation, and Education Counsel found the typical net price for graduate school (which includes tuition, fees, books, and living expenses, among other costs, less any federal, state, or institutional grant aid) increased from $18,500 in 1995 to $33,500 — a jump of 81 percent. 14 Anecdotally, the high price of graduate school helps to subsidize undergraduate education and back-fill budget challenges colleges face elsewhere in their operations, though little research exists on the extent of these cross-subsidies. 15

It also appears the creation of the Grad PLUS loan program enabled colleges to increase their prices. For instance, one recent study found the availability of Grad PLUS loans led institutions to increase their prices by more than 50 cents per $1 increase in federal borrowing. 16 Average graduate student debt levels also spiked after 2005, when the program began. 17

One recent study found the availability of Grad PLUS loans led institutions to increase their prices bymore than 50 cents per $1 increase in federal borrowing.

Graduate education returns are highly uneven, with some programs far more likely to pay off than others — and some less likely to pay off for students of color, in particular. The costs and outcomes of graduate programs vary considerably across fields. For instance, master’s and doctoral degrees in psychology, master’s degrees in visual and performing arts, and for-profit master’s or doctoral degrees in family and consumer sciences leave students with unaffordable debt or low earnings at particularly high rates. 18

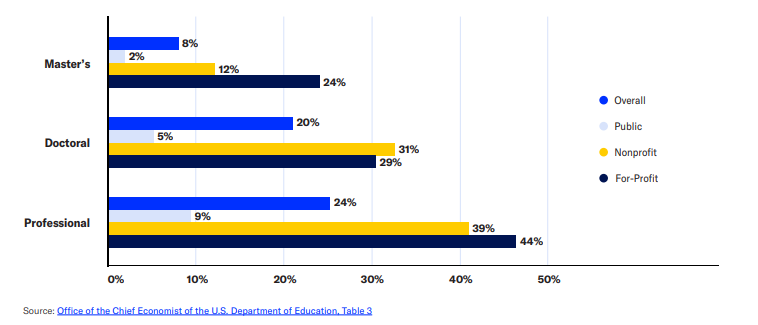

However, these outcomes also vary considerably from school to school, meaning students’ return on investment also varies significantly depending on the institution where they enroll. An analysis by the Education Department’s Chief Economist found that 8 percent of master’s degree programs leave graduates deeply indebted, with loans that exceed 8 percent of their annual income and 20 percent of their discretionary income. While that number is just 2 percent for master’s degree programs at public colleges, it jumps to 12 percent for nonprofit programs and 24 percent for for-profit programs. 19 Among professional degree programs, 24 percent are high-debt, ranging from 9 percent at public colleges to 44 percent at for-profit programs. 20 In fact, another analysis found that advanced degree graduates at more than one in seven programs are no better off than they would have been without graduate school, earning less than the average bachelor’s degree graduate. These graduate degrees also drain students of time and money they could have spent more fruitfully elsewhere. 21

Share of High-Debt-Burden Graduate Programs, By Degree Type and Sector

These uneven returns are most severe for students of color, particularly Black students. Black student enrollment in graduate education increased by nearly 80 percent from 2004 to 2012 — but more than half of that growth was in for-profit colleges, where debt-to-earnings rates are worst. The share of Black students in public colleges, where programs are much more likely to pay off, declined over a similar timeframe. 22 By 2020, about half of white and Hispanic graduate students were enrolled in graduate programs at public colleges and 10 percent at for-profit colleges. Fewer than 40 percent of Black graduate students were at public colleges, and more than 20 percent were enrolled at for-profits.

Policy Solutions

This proliferation of high-cost and/or low-return graduate education programs presents a continuing challenge in ensuring our higher education system provides real, tangible value to students and taxpayers. However, there are some common sense policy changes that can address and constrain the runaway costs for graduate education. Policymakers should act quickly to improve and enhance return on investment for these programs. Federal policy solutions include:

Increasing transparency into graduate education. Students pursuing graduate education may not be aware of the amounts they can expect to earn after completing their program, and especially of how their return on investment might vary from institution to institution. The College Transparency Act would ensure students have the data needed to make smart, informed decisions about the returns of specific education programs.

Capping graduate student lending. There is clear evidence that the Grad PLUS program, which offers students unlimited borrowing up to the school-determined cost of attendance, has led colleges to increase driven up graduate program prices without improving access. Multiple Congressional bills propose capping or even eliminating the Grad PLUS program, such as the College Cost Reduction Act from Rep. Virginia Foxx (R‑N.C.) 23 and the Graduate Opportunity and Affordable Loans Act from Senators Cassidy (R‑L.A.) and Tuberville (R‑A.L.). Policymakers should set a limit on Grad PLUS loans that accounts for varied earnings across fields of study and degree level. This would preserve broad access to high-return professional and health fields while limiting borrowing to amounts that students can realistically repay.

Ensuring students see real returns from their graduate programs by instituting program eligibility thresholds. Available data confirm that some programs simply provide too low a return on investment to be worth students’ time and money. Those programs should lose access to federal student loan eligibility. For instance, the Biden Administration promulgated regulations that would set a minimum debt-to-earnings rate for career-training programs (including for-profit graduate education programs), and would require students in other types of graduate programs to attest to the low ROI prior to enrolling in failing programs. 24 Sens. John Cornyn (R‑T.X.) and Bill Cassidy (R‑L.A.) went even further than those regulations, introducing legislation that would require all graduate programs to ensure they leave students better off than they would have been without the program, reporting typical earnings above those of someone with a bachelor’s degree. 25

It is time to codify these requirements in law, ensuring taxpayer dollars invested in higher education truly do advance students’ economic circumstances. In addition, institutions with too many low-performing graduate programs could also lose access to Grad PLUS loans altogether, ensuring they cannot continue to exploit students and taxpayers for persistently poor performance.

1

Monarrez, Tomás and Jordan Matsudaira, “Trends in Federal Student Loans for Graduate School,” U.S. Department of Education,Office of the Chief Economist, August 2023, https://assets.arnoldventures.....

Kelchen, Robert and Faith Barrett, “Exploring the Growth of Master’s Degree Programs in the United States,” Postsecondary Equity & Economics Research Project, April 2024, https://www.american.edu/spa/p...; and “A Framework for Reforming Federal Graduate Student Aid Policy,” American Enterprise Institute, EducationCounsel, and The Century Foundation, December 2023, https://www.nelsonmullins.com/....

“A Framework for Reforming Federal Graduate Student Aid Policy;” Kelchen, Robert and Faith Barrett, “Exploring the Growth of Master’s Degree Programs in the United States;” and Monarrez, Tomás and Jordan Matsudaira, “Trends in Federal Student Loans for Graduate School.”

“Interest Rates and Fees for Federal Student Loans,” Office of Federal Student Aid, U.S. Department of Education, available at: https://studentaid.gov/underst....

Delisle, Jason, “How Access to Federal Student Loans Could Change under the College Cost Reduction Act,” Urban Institute, June 2024, https://www.urban.org/sites/de...; and “Student Loans Overview: Fiscal Year 2025 Budget Proposal,” Congressional Justifications, U.S. Department of Education, https://www2.ed.gov/about/over....

Monarrez, Tomás and Jordan Matsudaira, “Trends in Federal Student Loans for Graduate School” (Table 1). Note that figures are adjusted to 2020 dollars.

Marcus, Jon, “Graduate Programs Have Become a Cash Cow for Struggling Colleges. What Does That Mean for Students?,” PBS News and The Hechinger Report, September 2017, https://www.pbs.org/newshour/e...

“Financial Value Transparency and Gainful Employment, Financial Responsibility, Administrative Capability, Certification Procedures, Ability to Benefit,” Proposed Rule, U.S> Department of Education, May 2023, https://www.regulations.gov/do... (Tables 3.6 and 3.10).

“Foxx Spearheads Legislation to Address Rising College Costs,” Press Release, House Committee on Education and the Workforce, U.S. Congress, January 2024, https://edworkforce.house.gov/....

“Biden-Harris Administration Announces Landmark Final Rules to Protect Consumers from Unaffordable Student Debt and Increase Transparency,” Press Release, U.S. Department of Education, September 2023, https://www.einpresswire.com/a...

“Ranking Member Cassidy, Colleagues Unveil Landmark Package to Lower Education Costs and Student Debt,” Press Release, Sen. Bill Cassidy, M.D., June 2023, https://www.einpresswire.com/a...; and “Streamlining Accountability and Value in Education (SAVE) for Students Act,” Fact Sheet, Sen. John Cornyn, June 2023, https://www.help.senate.gov/sa....