AV Issue Brief

The Tax Cuts and Jobs Act (TCJA) capped the SALT deduction at $10,000 per tax return. Prior to the TCJA, there was no explicit limit on this deduction, but the broader Alternative Minimum Tax (AMT) — which affected households with incomes as low as the low six figures — already served as an implicit cap on SALT deductions. The TCJA increased both the AMT exemption and the income level at which the AMT exemption phases out, so far fewer taxpayers pay the AMT—falling from 5 million in 2017 to about 200,000 in 2025. In fact, virtually no one earning under $1 million pays AMT as a result of the TCJA changes.

Using PolicyEngine’s SALT Calculator, we pulled examples from a handful of high-tax states, demonstrating that outside the highest of income earners, the pre-2018 AMT served as a de facto SALT cap — in most cases at amounts far below some of the proposals from advocates to raise the cap. Raising the SALT Cap, while extending the TCJA’s AMT relief, would provide some of the highest income earners in America with a more generous SALT deduction than they enjoyed before the TCJA.

When considering the extension of the SALT cap in 2025, it’s important to understand the interaction between the SALT cap and the AMT exemption.

Topline Takeaways:

- High-income taxpayers in high-tax states already faced a cap on their SALT deductions prior to the TCJA because the AMT limited their SALT deduction at a lower level than most realize.

- As a result, combining the TCJA’s higher AMT threshold and a more generous SALT cap could allow itemizers in high-tax states to deduct more SALT than they ever could.

- Families in high-tax states pay lower taxes under the One Big Beautiful Bill (OBBB)– considering the totality of the changes – than if the TCJA were allowed to expire. This includes the vast majority of taxpayers earning $250,000 to $500,000.

AMT as an Effective Cap On SALT

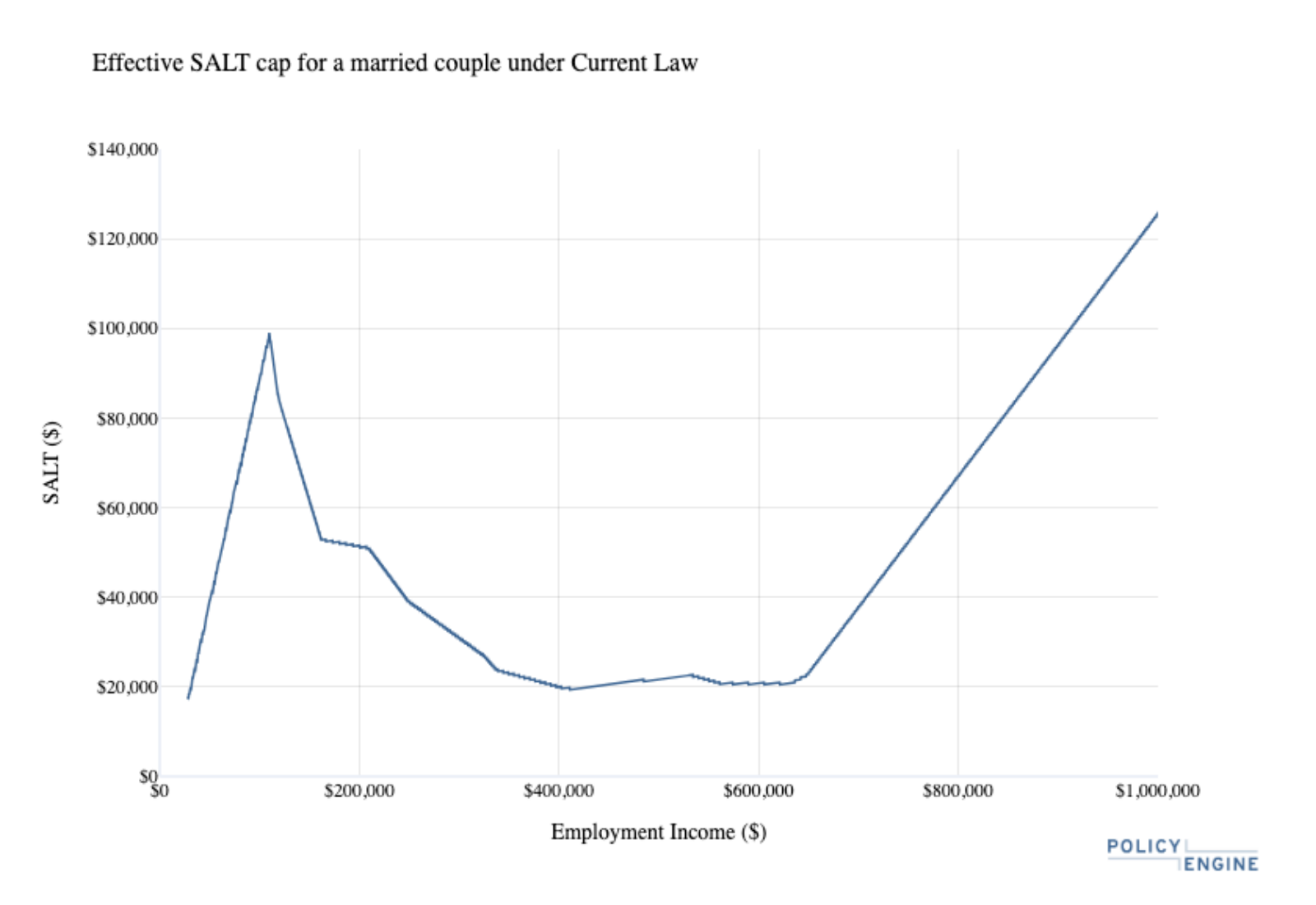

It’s not accurate to say that the SALT deduction was uncapped prior to the TCJA. When a taxpayer’s deductions— including SALT — became large enough, that taxpayer could be pushed into the AMT system. Prior to the TCJA, the AMT was structured to affect a much larger share of taxpayers, including many with middle-class incomes. The graph below illustrates how much the AMT would limit the SALT deduction for a married household in 2026 if the TCJA expires.

Subsidy for Only the Highest Earners

As the above example shows, for many upper-middle income earners, AMT already created a SALT cap of roughly $20,000 before TCJA. Households earning less than $100,000 or so could deduct unlimited SALT because they did not earn enough to pay AMT. But then the maximum SALT deduction declines rapidly to about $20,000 as income rises to about $400,000, because the AMT is phasing in. Only the very top sliver of income earners — those earning about $650,000 or more — could claim much above this amount.

Interacting Provisions

There are multiple interacting changes to the TCJA that shape the overall tax equation — not just the state and local tax (SALT) deduction cap and the alternative minimum tax (AMT). The TCJA significantly narrowed the scope of the AMT, doubled the standard deduction (reducing the number of itemizers), and suspended the Pease limit on itemized deductions. Each of these changes affect how taxpayers experience the SALT cap and interact with the AMT, meaning that adjusting one provision without considering the others could have unintended consequences.

Case Studies: SALT/AMT Interaction in Practice

PolicyEngine — an open-source tax modeling platform — created a calculator to help policymakers and individuals understand how these two provisions interact. Using the states of New York, New Jersey, and California as case studies, here are the impacts PolicyEngine’s calculator shows for some typical households:

Federal tax liability in 2026: Married couple filing jointly with one child

| Wage Income | ||

|---|---|---|

| Scenarios | $250,000 | $500,000 |

| CALIFORNIA | ||

| Current law (TCJA expiration) | $33,928 | $105,750 |

| House-passed OBBB, with 30k SALT Cap | $30,255 | $88,528 |

| Senate Finance OBBB, with 30k SALT Cap | $30,586 | $85,836 |

| Average property tax rate: 0.71% | ||

| Wage Income | ||

|---|---|---|

| Scenarios | $250,000 | $500,000 |

| NEW JERSEY | ||

| Current law (TCJA expiration) | $30,979 | $105,750 |

| House-passed OBBB, with 30k SALT Cap | $30,054 | $88,528 |

| Senate Finance OBBB, with 30k SALT Cap | $30,354 | $85,836 |

| Average property tax rate: 2.23% | ||

| Wage Income | ||

|---|---|---|

| Scenarios | $250,000 | $500,000 |

| NEW YORK | ||

| Current law (TCJA expiration) | $32,109 | $105,750 |

| House-passed OBBB, with 30k SALT Cap | $30,054 | $88,528 |

| Senate Finance OBBB, with 30k SALT Cap | $30,354 | $85,836 |

| Average property tax rate: 1.6% | ||

All figures assume a household married filing jointly with one child. Filers have 90th percentile of itemized deductions of joint filers with wages within 10% of the value, regardless of state and children, per PolicyEngine’s 2026 Enhanced current Population Survey. This is equal to $250,000 in wage income, and $57,000 for $500,000 in wage income. Property tax rates are state averages, and home prices are derived from the median home price to income ratio of 5.6 to 1.

Families earning $250,000 or $500,000 consistently pay less tax under the both the House- and Senate-passed OBBB, even with a $30,000 SALT cap, than if the TCJA expires. With TCJA permanence and an increase in the SALT cap to $30,000, they pay far less tax than they did either under the TCJA ($10,000 SALT cap) or before the TCJA (under an AMT-imposed effective SALT cap). Notice also that by the time income rises to $500,000, federal income tax liability is the same regardless of where the taxpayer resides, both under current law and under current policy. This occurs because, regardless of whether we are dealing with a SALT cap of $30,000 or the old AMT, taxpayers have hit their limit on how much SALT they may deduct by the time they reach this income level.

Resources

- How SALT May Shake Up the 2025 Tax Debate | Bipartisan Policy Center

- 2017 Tax Changes Increase the Benefit of Uncapping SALT Deductions for High Income Taxpayers | Tax Foundation

- Revisiting the State and Local Tax Deduction | Tax Policy Center

- A Guide to the SALT Cap Debate | TaxNotes